Maturity of commercialization of humanoid robotics by application. For full data, refer to IDTechEx’s research on “Humanoid Robots 2026-2036: Technology, Market, and Opportunities”

This blog post was originally published at IDTechEx’s website. It is reprinted here with the permission of IDTechEx.

Automotive industry, logistics, home-use, key players and suppliers, AI chip, battery, actuator, motor, screw, tactile sensor, camera, bearing, LiDAR, PEEK materials, cost analysis of components, 10-year volume and market size forecast

Humanoid robots are increasingly viewed less as futuristic prototypes and more as a concrete way to bring artificial intelligence into human-designed environments, enabled by advances in embodied AI, more capable electromechanical hardware, and growing demand for flexible automation in labor-constrained industries. Over the last 12 months, activity has shifted from trade-show demonstrations to structured pilots on production sites, supported by larger, more deliberate investment from both venture-backed startups and established OEMs. With component supply chains gradually stabilizing and early cost reductions coming through, operators are starting to use real deployment data to define where humanoids are viable, and where they are not, in the near term.

IDTechEx’s report, “Humanoid Robots 2026-2036: Technologies, Markets, and Opportunities”, provides a detailed technical and commercial assessment of humanoid robots at the component level. It covers actuators, motors, reducers, screws, bearings, cameras, LiDAR, radar, ultrasonic sensors, tactile sensors, software and AI stacks, batteries, thermal management, high-performance materials, and end effectors. The report evaluates design and manufacturing challenges, cost-down potential, supply chain constraints, and the realistic adoption trajectory across key industries.

Key Insights from the Report

- 10-year market size forecast (2026-2036) for humanoid robots, segmented by automotive, logistics/warehousing, and home-use applications

- 10-year volume/unit shipment forecast (2026-2036) for humanoid robots across key industries

- Component-level market sizing and forecasts for major humanoid hardware subsystems, including actuators, motors, reducers, screws, bearings, cameras, LiDAR, radar, ultrasonic sensors, tactile sensors, batteries, and structural materials

- Component-level volume forecasts supporting supply chain scaling analysis

- Battery capacity (MWh) forecast and assessment of runtime limitations, charging downtime, and emerging hot-swappable battery approaches

- Average selling price (ASP) forecast and cost-down roadmap, highlighting key cost drivers and bottlenecks

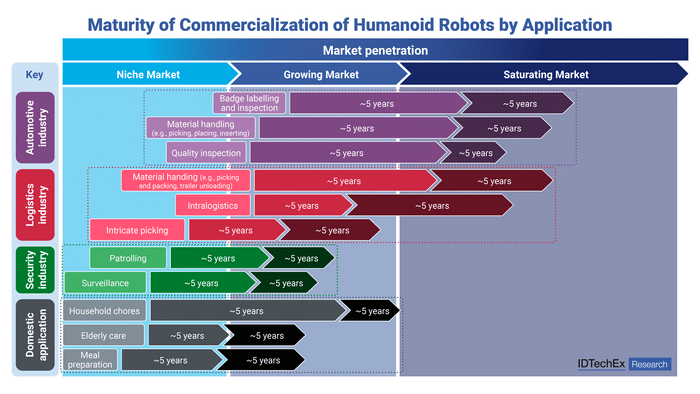

Industrial Adoption: Automotive and Logistics as the First Scaling Markets

IDTechEx expects automotive manufacturing to be the first market segment to scale humanoid robot deployment. This is driven by strong strategic backing from OEMs, controlled operating environments, and clearer ROI justification for repetitive labor-intensive tasks. Early deployments are focused on basic but scalable tasks such as material handling, inspection support, intra-factory transport, and simple assembly assistance, with increasing emphasis on reliability, safety validation, and maintainability rather than “general-purpose” capability.

Logistics and warehousing adoption are expected to follow, although growth may be moderated by competition with existing automation solutions such as AMRs, AGVs, and robotic arms. However, humanoid robots are increasingly positioned as a flexible alternative where mixed tasks are required in environments designed around humans. As hardware cost declines and task performance improves, humanoids could become commercially attractive for basic pick-and-place, parcel handling, and repetitive warehouse workflows.

Home-use humanoid robots remain a longer-term opportunity. While penetration is expected to remain limited within the 2026-2036 forecast window, IDTechEx believes this segment will remain strategically important due to its potential long-term demand scale, once safety, affordability, and reliability barriers are addressed.

Component-Level Challenges: Cost, Reliability, and Supply Chain Bottlenecks

Despite accelerating market momentum, humanoid robots still face major engineering and manufacturing constraints. Key bottlenecks include battery energy density and thermal management limitations, which restrict operating time and increase downtime. At the same time, scaling high-precision components such as screws, bearings, and high-performance actuators remains a critical challenge, as current supply chains are not yet optimized for mass-volume humanoid production.

Dexterous hands and tactile sensing also remain a major hurdle for expanding humanoid task capability beyond simple industrial operations. The report assesses the current state of end effector design, tactile sensor maturity, and software integration requirements, highlighting which technical pathways are most likely to scale commercially.

Conclusion

Humanoid robots are moving beyond hype-driven prototypes toward early commercial deployment, with automotive manufacturing emerging as the first scalable adoption market. Logistics and warehousing are expected to follow as cost declines and performance improves, while home-use remains a longer-term strategic demand driver. With continued progress in embodied AI and hardware cost reduction, IDTechEx forecasts the humanoid robot market will reach ~US$29.5 billion by 2036.

Key Aspects

This report provides critical market intelligence about humanoid robots, focusing on their major applications and each component’s technical, regulatory, and commercial challenges. This includes:

A review of state-of-the-art humanoids, their target industries, and adoption timeline:

- Current task and industry of humanoid robot, including automotive industry and warehousing/logistics industry

- General overview of important technologies within each sector

- Benchmarking and analysis of different humanoid robot players

Full analysis of each hardware component of the humanoid robot:

- Technical analysis and challenges of components, including actuators, motors, reducers, screws, bearing, cameras, LiDAR, radar, and ultrasonic sensors, tactile sensors, software and AI, battery, high-performance materials, and arm effectors

- Cost analysis of different components

- Design and manufacturing challenges

- Regulatory challenges

- Future trends of critical components and key technologies to be used

Market size forecast and business opportunities throughout:

- Reviews of humanoid robot players throughout the automotive industry and the logistics/warehousing industry

- Historic humanoid robot market data from 2023-2025

- Cost forecast of humanoid robot from 2026-2036.

- Market size and adoption volume forecasts from 2026-2036 for the automotive industry, Home-use and logistics/warehousing industry

- Market size and adoption volume forecasts from 2026-2036 for main components used in humanoids, including actuators, motors, reducers, screws, bearing, cameras, LiDAR, radar, and ultrasonic sensors, tactile sensors, software and AI, battery, high-performance materials, and arm effectors

- Battery capacity forecast from 2026-2036 for humanoid robots

Analyst access from IDTechEx

All report purchases include up to 30 minutes telephone time with an expert analyst who will help you link key findings in the report to the business issues you’re addressing. This needs to be used within three months of purchasing the report.

Further information

If you have any questions about this report, please do not hesitate to contact our report team at [email protected] or call one of our sales managers:

AMERICAS (USA): +1 617 577 7890

ASIA (Japan and Korea): +81 3 3216 7209

ASIA: +44 1223 810259

EUROPE (UK) +44 1223 812300

Shihao Fu, Technology Analyst, IDTechEx