The transition toward software-defined ADAS platforms is reshaping supply chains, accelerating ecosystem transformation, and redefining industry leadership.

Key Takeaways

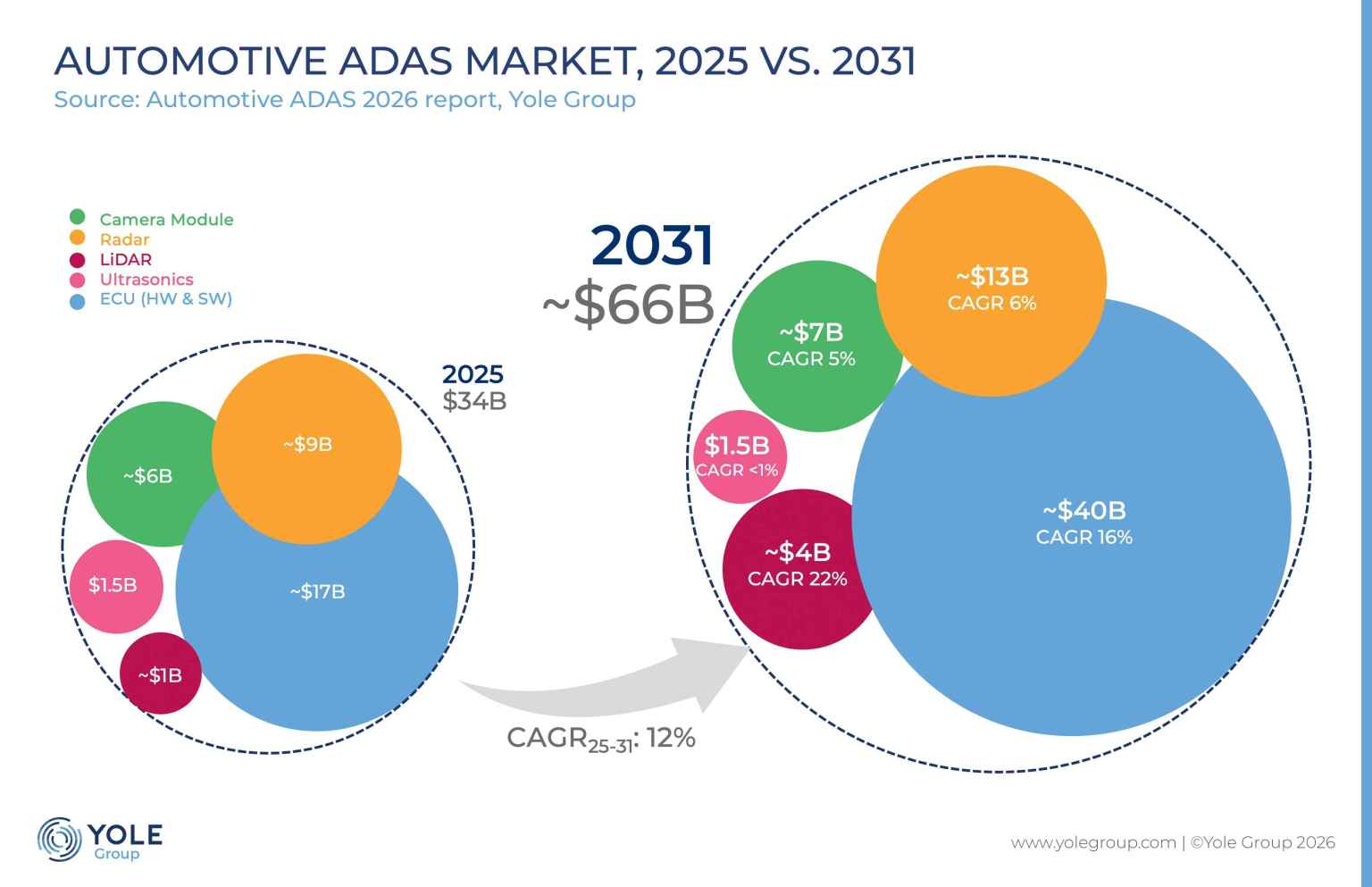

- The ADAS market is set to grow to more than $66 billion by 2031, with value shifting from sensors to computing.

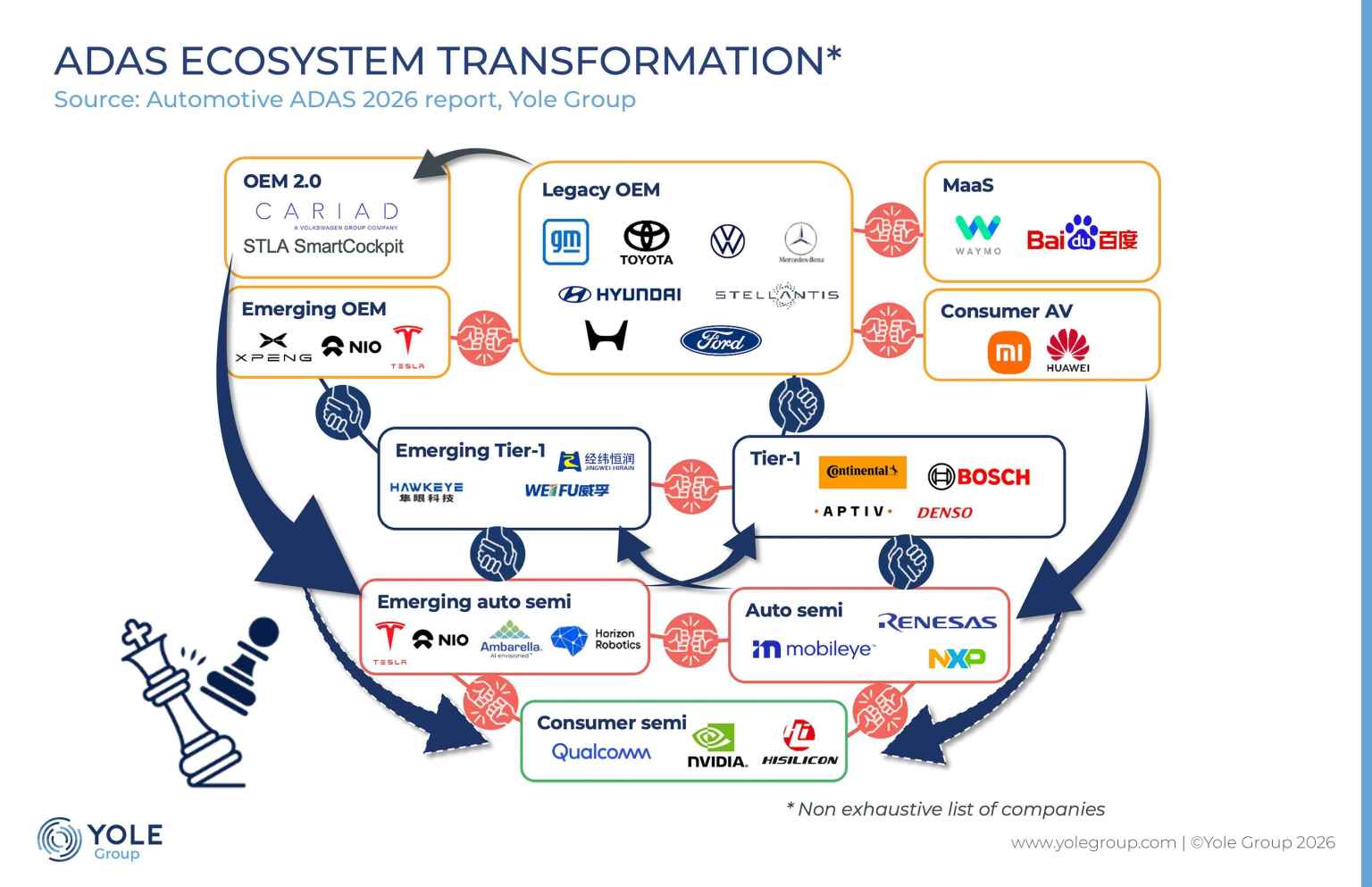

- Supply chain: China is emerging as the fastest-growing and most dynamic ADAS ecosystem, reshaping global competition. Yole Group sees new roles across OEMs, Tier-1s, and semiconductor players: control is moving toward compute platforms and software integration.

- Sensor innovation continues, but differentiation increasingly depends on integration within centralized, software-defined architectures.

Yole Group announces the release of its latest market and technology report, Automotive ADAS 2026, providing a comprehensive analysis of a rapidly evolving industry entering a new phase of growth and transformation.

As vehicles become increasingly software-defined, ADAS is no longer driven solely by the proliferation of sensors. Instead, the market is transitioning to integrated platforms combining sensing, centralized computing, and software. This shift is redefining value creation across the automotive ecosystem and accelerating the convergence between hardware and software capabilities.

Pierrick BOULAY, Principal Technology & Market Analyst, Automotive Semiconductors, at Yole Group: “The ADAS market is entering a new phase where value is no longer driven by the proliferation of sensors, but by the ability to integrate sensing, computing, and software into scalable platforms. This transition is fundamentally reshaping how the industry creates and captures value.”

According to Yole Group’s analysis, the global ADAS market, including sensors and electronic control units, is expected to grow to more than $66 billion by 2031. While sensor demand remains strong, the fastest growth is now concentrated in computing platforms and software, reflecting the industry’s shift toward domain and centralized architectures.

Yole Group’s report highlights a fundamental transition from a sensor-centric approach to a system-level perspective. Cameras remain the backbone of ADAS deployments, while radar technologies are evolving toward higher-resolution imaging solutions, and LiDAR is experiencing the fastest growth, particularly for long-range applications. However, the true differentiation increasingly lies in how these sensing modalities are orchestrated through software and computing platforms.

Centralized computing architectures are progressively replacing distributed electronic control units, enabling higher processing performance, improved scalability, and more efficient system integration. As a result, software content and system-level optimization are becoming critical levels of competitiveness.

This transformation is significantly impacting the automotive supply chain. “Traditional Tier-1 suppliers are expanding beyond hardware delivery to system integration, software enablement, and validation,” asserts Pierrick Boulay from Yole Group. “At the same time, semiconductor companies are moving up the value chain by building closer relationships with OEMs and offering more complete platform solutions.”

One of the key insights in Yole Group’s new report is the emergence of China as a distinct and highly dynamic ADAS market. Characterized by rapid deployment of enhanced features, strong local supply chains, and vertically integrated ecosystems, China is accelerating both innovation cycles and adoption rates, particularly for advanced L2+ driver assistance systems. China is accelerating ADAS innovation, while control of software and compute becomes the key battleground.

As the ADAS industry enters this new software-defined era, understanding the evolving balance between sensing, computing, and software integration becomes critical for all automotive players. Yole Group’s Automotive ADAS 2026 report provides key insights into the technologies, ecosystems, and competitive dynamics shaping the road ahead.